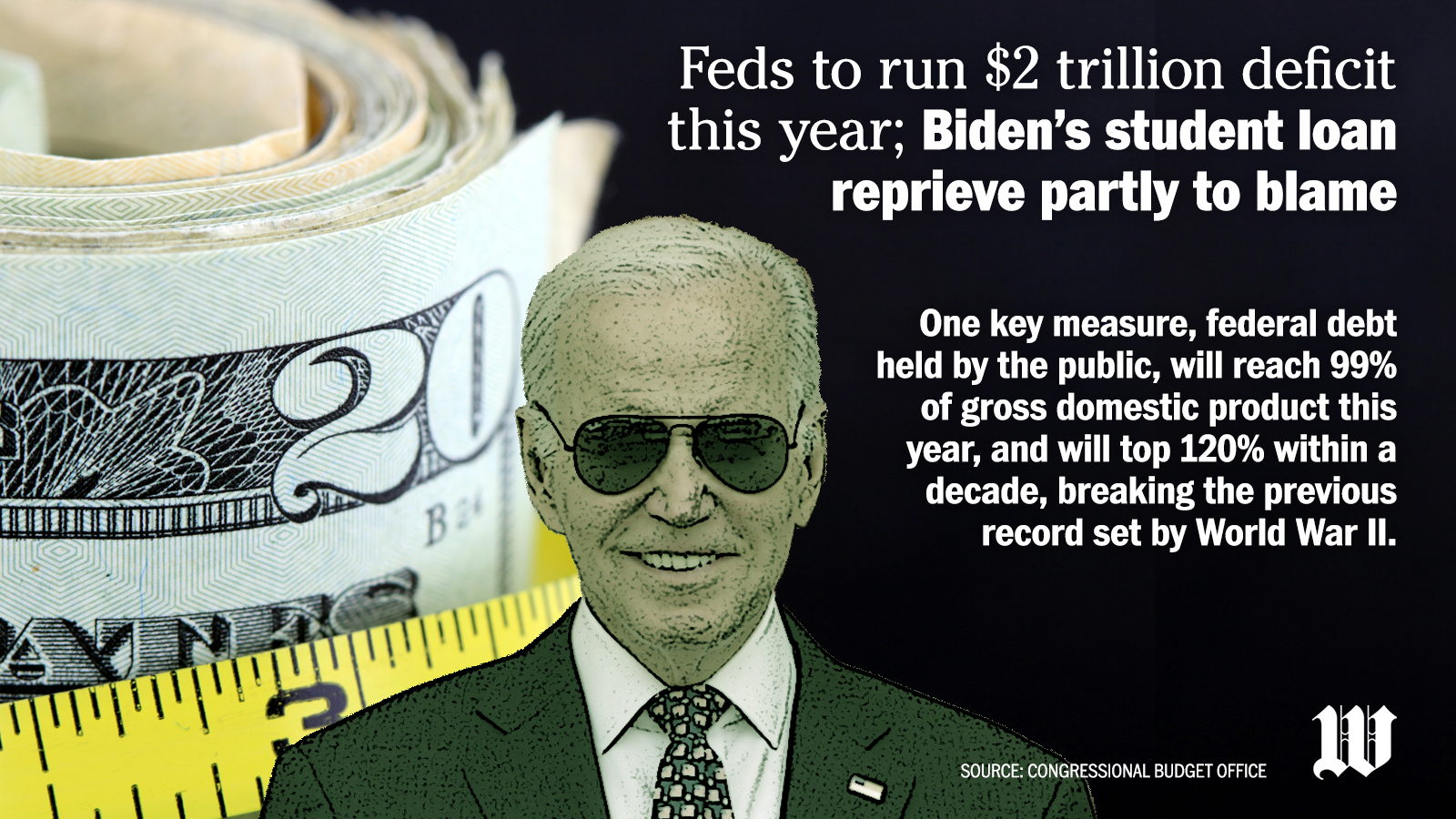

The federal budget deficit will reach $2 trillion this year, the Congressional Budget Office said Tuesday, laying at least part of the blame on President Biden’s generous student loan forgiveness plans.

The good news is that the economy continues to hum along, fueled in large part by the record numbers of migrants surging into the U.S., legally or otherwise. CBO said it has upgraded its economic growth and unemployment numbers over the last four months.

Inflation remains high, mooting some of the gains.

CBO said its deficit estimate increased by $400 billion in the last four months as Congress approved war spending for Ukraine and Israel, Medicaid costs rose faster than anticipated, and Mr. Biden wrote off a significant chunk of Americans’ outstanding student loan debt.

The result is a spreading sea of red ink.

One key measure, federal debt held by the public, will reach 99% of gross domestic product this year, and will top 120% within a decade, breaking the previous record set by World War II.

“Then it continues to rise,” said CBO Director Phillip L. Swagel.

The grim projections come in the middle of a heated political campaign season, and ahead of an expected debate next year over how — or whether — to extend the tax-cut package that then-President Trump signed into law in 2017.

Voters right now don’t seem to be paying much attention to spending and the debt, but inflation is a top issue.

Republicans said the report is a rebuke to Democrats’ spending plans. Democrats saw the report as ammunition to use against the GOP’s hopes of extending the tax cuts.

Michael A. Peterson, CEO of the watchdog Peter G. Peterson Foundation, pleaded with voters to demand better from all sides.

“This November, America’s fiscal and economic future is on the ballot, and voters are calling for leaders who will prioritize solutions to our growing debt,” he said.

Voters aren’t particularly irked by spending and debt but the inflation does hit home.

CBO said things aren’t likely to improve much on that score before the election. The personal consumption expenditures price index will fall from 2.8% at the end of last year to 2.7% by the end of this year, and the consumer price index growth will drop from 3.2% to 3.0%.

Inflation-adjusted gross domestic product will grow 2% this year, down from 3.1% in 2023 but still impressive for an economy that was given a 100% chance of going into recession last year.

CBO said a large part of that resilience is because of what it described as “a surge in immigration that began in 2021,” and which CBO figured will last at least through 2026.

The analysts figure the U.S. netted 2.4 million new immigrants last year and will see 2.4 million more this year.

Most of those are what CBO terms “other foreign nationals” — people who aren’t here as guest workers or permanent immigrants. They are largely made up of parolees and immigrants who lack a legal visa.

CBO said the higher rates of immigration will add nearly $9 trillion to GDP over the coming decade, or about 2.4%. That means more tax revenue, but also higher spending as the immigrants push up inflation rates and the government has to spend more on interest costs on the national debt.

While the news is generally good for the economy as a whole, it’s not so good for the average worker, particularly those on the lower economic rungs.

“Increases in the supply of workers put downward pressure on wages, particularly for people with 12 or fewer years of education,” CBO concluded.

On the budget side, there’s plenty of record-breaking news, and it’s mostly bad. CBO said that’s all the more worrying because the economy and jobs pictures have been so good.

Deficits will top 5.5% of GDP every year over the next decade. The annual average for the last 50 years has been 3.7%.

Uncle Sam will spend nearly $900 billion on interest payments alone this year, rising to $1.7 trillion in 2034. Never before, in records dating back to 1940, has the government spent such a high ratio of its GDP on debt-interest payments.

Debt held by the public will nearly double over the next decade, from $26.2 trillion as of 2023 to $50.7 trillion by 2034.

Federal spending will average 4% increases each year over the coming decade, with Social Security and Medicare accounting for most of that.

This year alone, Mr. Biden’s latest attempt at student loan forgiveness is adding tens of billions of dollars to the deficit.

• Stephen Dinan can be reached at sdinan@washingtontimes.com.

Please read our comment policy before commenting.