As tensions heat up between Iran and the West, the prospect of a big spike in oil prices to as high as $200 a barrel suddenly looms over the U.S. economy, threatening to overshadow what have been promising signs of gathering strength.

U.S. consumers have proved highly sensitive to the price of fuel, which shot up recently after Iran threatened to close the Strait of Hormuz — the only exit from the oil-rich Persian Gulf for one-fifth of the world’s oil exports.

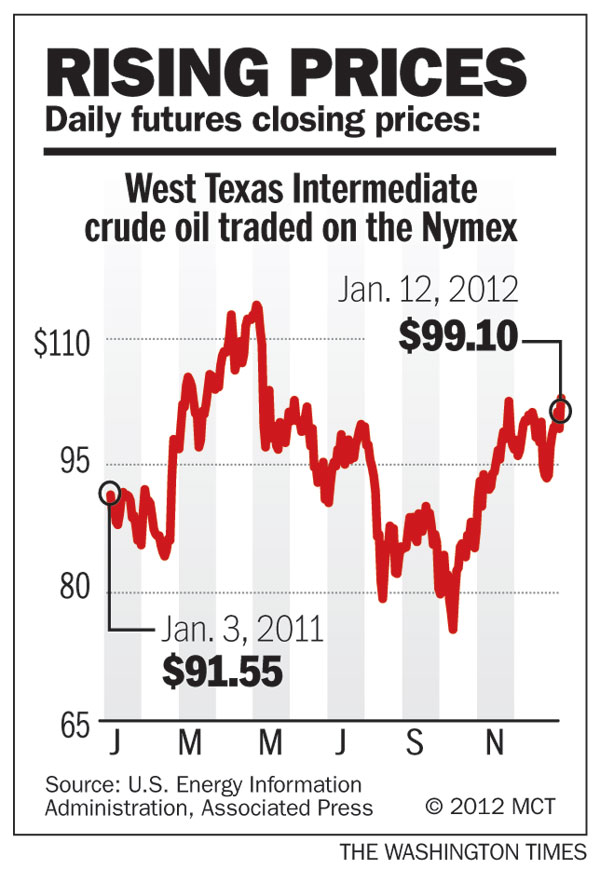

At about $3.28 a gallon at the pump, regular gasoline prices are at record levels for this time of year and are likely to go up as demand rises in the months ahead. The renewed pressure on gas prices could prompt consumers who opened their wallets during the critical Christmas shopping season to pull back on spending, imperiling the economy as they did last year when high oil prices sent gasoline to uncomfortable levels close to $4 per gallon and nearly snuffed out economic growth.

Analysts generally think Iran is bluffing and is unlikely to risk a military confrontation with the U.S. by blocking the critical passageway for oil shipments — including those vital to Iran’s economy — but no one can rule out the possibility that Iran’s deeply anti-American rulers will make good on their threats.

“Closure would do far more damage to Iran in economic terms than the sanctions” the West is preparing to impose on Iran for refusing to abandon its nuclear ambitions, said Frank A. Verrastro, senior vice president at the Center for Strategic and International Studies.

“Closure would do far more damage to Iran in economic terms than the sanctions” the West is preparing to impose on Iran for refusing to abandon its nuclear ambitions, said Frank A. Verrastro, senior vice president at the Center for Strategic and International Studies.

By all accounts, Iran’s economy al ready is suffering greatly in anticipation of a round of sanctions that are the broadest ever to be imposed on Tehran. With the nation’s currency plummeting and causing financial and economic turmoil, Iran’s leaders have been casting about for ways to strike back at the West.

“Desperate nations driven to the brink sometimes do desperate and unpredictable things,” Mr. Verrastro said. “Even if short-lived, disruption to shipping in the Gulf would undoubtedly wreak havoc in oil markets.”

Energy analysts say premium crude prices would quickly double to $200 per barrel or higher if a military clash were to erupt in the Gulf. Such stultifyingly high prices, in turn, would deal a potentially devastating blow to the fragile economic recovery in the U.S. and likely throw Europe into a deep recession. The U.S. economy nearly came to a standstill in the wake of a much smaller oil shock last year caused by the Arab Spring uprisings across the Middle East.

“If the Straits of Hormuz close, oil will rise above $200 per barrel,” said Chris Faulkner, chief executive officer of Breitling Oil and Gas. “It’s the one bottleneck that allows Iran to choke the West’s oil supply.”

Other analysts point out that Iran has frequently threatened to hold the West hostage by closing the strait, without following through.

“This is the umpteenth time” Iran has made such a threat and it should be taken with a grain of salt once again, said Foreign Policy magazine columnist Michael A. Cohen. As in past episodes, the U.S. military is more than capable of overwhelming any attempts by Iran to follow through, he said.

“Iran is at best a second-rate power, with an outdated and not terribly advanced conventional military force that is barely able to project power outside its borders,” he said.

Nevertheless, as Iran’s leaders are well aware, often the mere threat of a blockade suffices to drive up oil prices to threatening levels.

Analysts estimate that the current price of oil includes a “risk premium” of $20 to $40 a barrel because of the recurring instability in the Middle East.

Iran’s threat is credible enough that the International Energy Agency has made contingency plans to release millions of barrels of oil from storage wells in the U.S., Europe and Japan. The Obama administration last year joined in a small release of oil from the strategic reserves to counter shortfalls of Libyan oil in world markets. Iran exports 2.4 million barrels a day.

Iran’s strenuous efforts to strike back at the U.S. are the result of the ratcheting up of economic sanctions this year to a point where they are now causing serious pain for Iran’s economy and citizens, analysts say.

For the first time, the U.S. is threatening to impose sanctions on companies that do business with Iran’s central bank, deploying the broadest and most potent tool available to hobble Iran’s economy. The mere threat of such sanctions have thrown Iran’s markets into turmoil.

Moreover, the European Union is cooperating with the latest round of sanctions — potentially cutting off as much as one-fifth of Iran’s oil sales in what would be a stunning blow to Iran’s economy.

Reports on Thursday that the EU will delay its embargo of Iranian oil sales by six months to allow European nations more time to find alternative sources of crude caused oil prices to fall below $100 a barrel for the first time this year, a sign of how sensitive market prices are to the latest political twists and turns.

The U.S. has encouraged other nations to find new suppliers of oil in a bid to make the sanctions stick. In addition, to prevent Iran from diverting sales of oil from Europe to Asia, which currently consumes about 60 percent of Iran’s exports, the U.S. has appealed to big Asian oil importers such as Japan and China to cooperate. Treasury Secretary Timothy F. Geithner made a round of visits in Asian capitals this week to try to persuade nations to come on board.

While China continues to resist curbing its oil trade with Iran, insisting that such commercial matters should not be caught up in the debate over Iran’s nuclear programs, the U.S. is likely to get broader cooperation with the sanctions this time around because alternative oil supplies are being made available by Saudi Arabia, which has grades of crude that are comparable to those exported by Iran, said Jeffrey J. Schott, an analyst with the Peterson Institute for International Economics.

Chinese Premier Wen Jiabao is set to begin his own five-day tour of the Middle East this weekend, bypassing Iran to visit Saudi Arabia, Qatar and the United Arab Emirates. The trip comes as Saudi Arabian Oil Co. and China Petroleum & Chemical Corp. sign an agreement for a proposed refinery on the Red Sea coast — Beijing’s first direct investment in a Saudi oil facility.

The increased flexibility for U.S. allies to get crude from Saudi Arabia combines with the greater effectiveness of broad sanctions on the financial sector to pose a potent threat to the Iranian government, which depends on oil sales for most of its revenue, Mr. Schott said.

“This really is a big ratcheting-up of the pressure on Iran, and it could lead to big political backlash from Iran,” he said. Tehran could try using military or covert operations against the West in retaliation as well as threatening to block the straits, he said. “We have to be prepared for that type of reaction.”

Because of the danger to the U.S. and world economies from a huge spike in oil prices, the law gives President Obama the flexibility to waive or postpone the sanctions later this year if he determines they would endanger U.S. economic growth, Mr. Schott said.

“If he thinks sanctions would cause a major spike in oil prices, he wouldn’t do it,” the analyst predicted.

• Patrice Hill can be reached at phill@washingtontimes.com.

Please read our comment policy before commenting.